Okay, let's break down Zakat calculation on different income streams – legally, ethically, and within the bounds of Islamic principles. This is crucial for maximizing your Zakat benefits (both spiritual and potential tax advantages, where applicable).

4. Properly Calculate Zakat on Diverse Income Streams

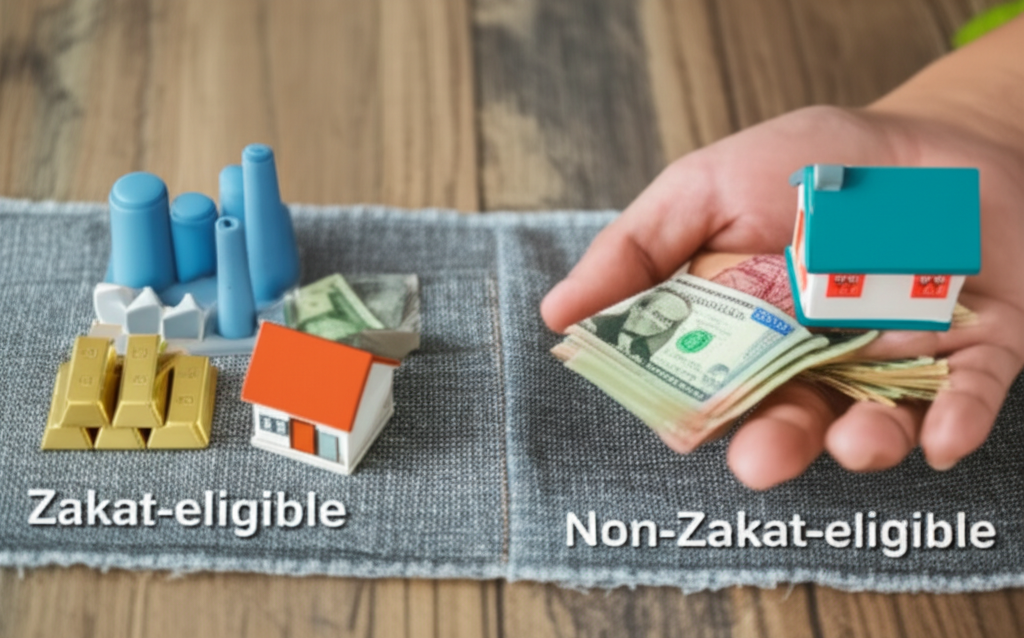

The modern economy involves a tapestry of income sources, so a one-size-fits-all Zakat calculation simply won't do. Understanding the nuances of each stream ensures you're fulfilling your obligation accurately. Don't leave it to guesswork!

Firstly, salary and wages are generally treated as income subject to Zakat. Most scholars agree that if your annual salary reaches or exceeds the Nisab (the minimum threshold), then 2.5% is due on the Zakatable amount. Deduct any essential expenses like housing, food, and debt from your total salary before calculating Zakat.

Business income presents a different challenge. This includes profits from your business, investments, or any other form of self-employment. You'll need to calculate your net profit (revenue minus expenses) for the Zakat year. Once you have this, again, if it meets or exceeds the Nisab, then 2.5% is typically due.

Rental income follows a similar principle to business income. Calculate your total rental income, deduct expenses like property taxes, maintenance, and management fees, and then apply the 2.5% Zakat rate to the net profit if it meets the Nisab. Remember to consult with a trusted Islamic scholar to verify which expenses are deductable.

Investments like stocks, bonds, and mutual funds can be tricky. Generally, Zakat is due on the market value of the investment at the end of the Zakat year if the investment is held for trade. If it is a long-term investment, Zakat is only due on the dividends or profits earned, not the entire asset. Seek advice from a scholar specializing in Islamic finance.

Freelance income is treated similar to business income. Track all your earnings and deduct legitimate business expenses (software subscriptions, marketing costs, etc.). Calculate Zakat on the net profit, ensuring it's above the Nisab.

Other income sources could include pensions, royalties, or even inheritance. How these are treated for Zakat purposes varies. Consult with a knowledgeable Islamic scholar for guidance to ensure that you are meeting your obligations.

Remember the Nisab! This is the minimum threshold of wealth that triggers the Zakat obligation. It's currently equivalent to the value of 85 grams of gold or 595 grams of silver. Keep an eye on fluctuating gold and silver prices to accurately determine your Nisab value for the year.

Finally, meticulously track all your income streams and expenses throughout the Zakat year. This accurate record-keeping is crucial for correctly calculating your Zakat obligation and ensuring you are giving what is due.